Understanding Lower Carbon Capital in Today’s Energy Landscape

Lower carbon capital represents the strategic allocation of investment funds toward projects, companies, and infrastructure that reduce greenhouse gas emissions while generating competitive financial returns. It’s not philanthropy or impact investing at concessionary rates—it’s the recognition that decarbonization creates genuine economic value.

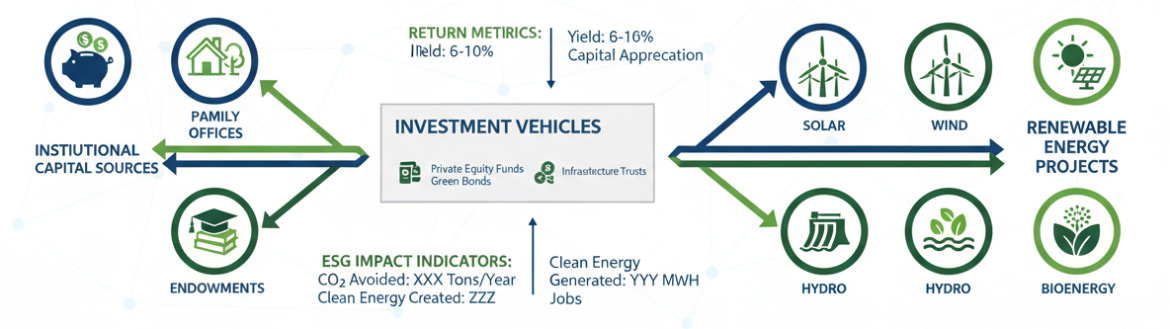

The scale of opportunity has matured considerably. Global markets have already mobilized over $13 billion in dedicated lower carbon capital, signaling that this approach has moved well beyond experimental phases. Institutional investors now view decarbonization not as a values-driven constraint but as a core investment thesis supported by regulatory momentum, technological advancement, and shifting consumer preferences.

Pension funds, endowments, and family offices are restructuring portfolios with explicit carbon reduction targets. Their rationale combines fiduciary responsibility with climate risk management. Stranded asset risk in fossil fuel infrastructure has become quantifiable, while clean energy technologies have achieved cost parity—and in many cases, cost advantages—over conventional alternatives.

The financing models that emerged from early pioneers have now become industry standards. Project finance structures for utility-scale solar and wind installations follow established playbooks. Yieldcos provide liquidity for operational assets. Growth equity supports scaling companies through commercialization barriers. These frameworks allow institutional capital to flow efficiently into climate solutions.

Hudson Sustainable Group’s investment approach demonstrates how sophisticated capital deployment across multiple asset classes can accelerate the energy transition while meeting institutional return requirements. Lower carbon capital isn’t a niche strategy anymore—it’s becoming the foundation for long-term value creation in the evolving energy economy.

What Lower Carbon Capital Means for Institutional Investors

For institutional investors, lower carbon capital represents more than environmental credentials—it’s a strategic reallocation of investment portfolios toward assets that generate reliable returns while reducing carbon exposure. This approach encompasses renewable energy infrastructure, sustainable transportation, energy efficiency projects, and grid modernization technologies that form the backbone of the global energy transition.

The asset classes within this space offer compelling characteristics that traditional portfolios often lack. Solar and wind farms provide predictable cash flows through long-term power purchase agreements. Battery storage systems capitalize on grid stability needs. Green hydrogen infrastructure positions investors at the forefront of industrial decarbonization. Each represents tangible, revenue-generating assets with clear pathways to profitability.

What separates theoretical interest from actual deployment is performance. Real-world evidence demonstrates that lower carbon capital strategies can deliver lifetime internal rates of return exceeding 31%, challenging the outdated notion that sustainability requires sacrificing returns. These aren’t projections—they’re documented outcomes from operational projects across multiple geographies and technologies.

Geographic diversification amplifies risk-adjusted performance. Spreading investments across 26 countries mitigates regulatory uncertainty, currency fluctuations, and regional market dynamics. A portfolio spanning U.S. solar developments, Japanese offshore wind, and European grid infrastructure captures growth across different regulatory environments and market maturity stages.

For pension funds and endowments, lower carbon capital directly addresses fiduciary obligations. These investments align with long-term return requirements while managing climate-related financial risks that threaten traditional holdings. ESG mandates aren’t constraints—they’re frameworks for identifying opportunities in sectors receiving substantial policy support. The right policy frameworks create the stable investment environment that institutional capital requires.

This isn’t about values over value. It’s about recognizing where capital formation is heading and positioning portfolios accordingly. The energy transition represents one of history’s largest infrastructure buildouts, and institutional investors who understand lower carbon capital strategies are capturing that growth.

Proven Financing Models Driving the Renewable Energy Sector

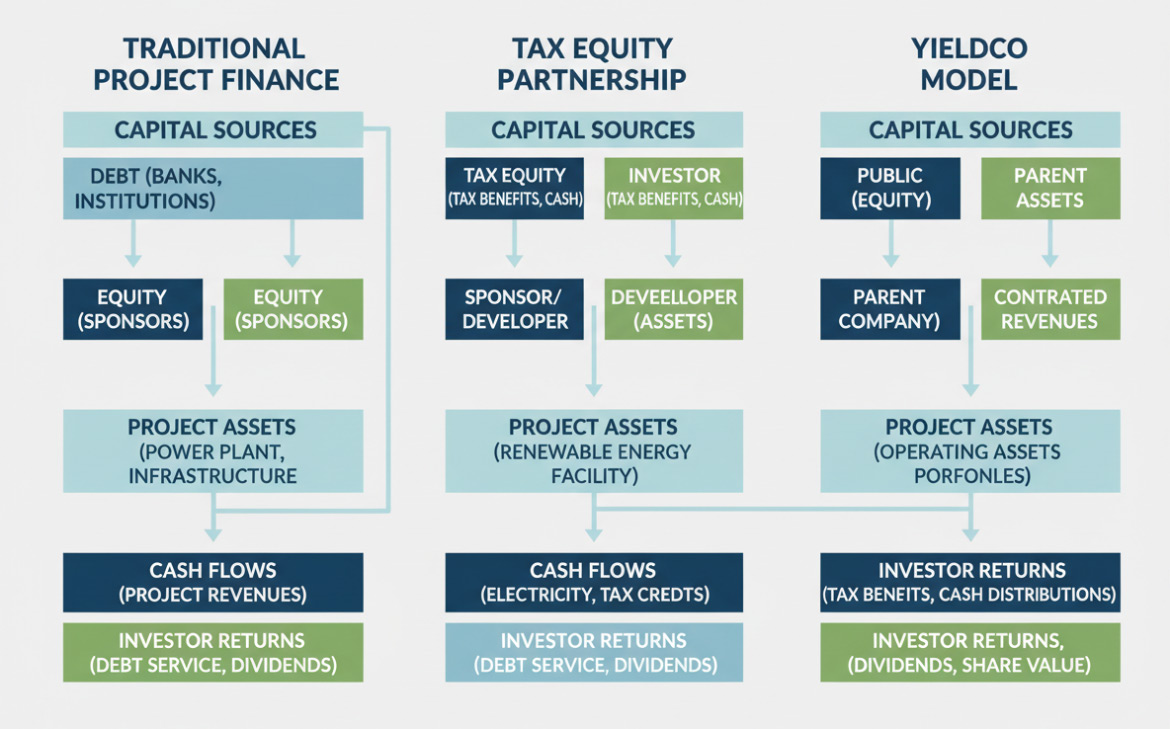

The renewable energy sector’s maturation over the past decade hasn’t happened by accident—it’s been built on increasingly sophisticated financing structures that make projects bankable at scale.

Tax equity partnerships transformed the industry’s early growth trajectory. These arrangements pair developers with institutional investors who can utilize federal tax credits, enabling projects that wouldn’t otherwise pencil out. The model’s proven so effective that it now channels tens of billions annually into solar and wind deployment. Recent IRA clean energy tax incentives have expanded these structures further, introducing transferability and direct pay options that broaden the investor base.

Yieldco structures emerged as another breakthrough, packaging operational renewable assets into publicly traded vehicles that deliver predictable cash flows to infrastructure investors. By separating stable, cash-generating assets from development-stage risk, yieldcos opened institutional capital markets to renewable energy in ways previously reserved for traditional utilities.

Perhaps the most significant innovation has been the corporate power purchase agreement. Companies like Amazon, Google, and Microsoft pioneered long-term offtake contracts that provide revenue certainty, making projects financeable without traditional utility involvement. These PPAs fundamentally changed project risk profiles—lenders now see 15-year contracts with investment-grade counterparties instead of uncertain merchant power exposure.

What started as experimental approaches have become standard practice. Project finance structures today routinely blend tax equity, institutional debt, and corporate offtake agreements into packages that attract lower carbon capital at competitive rates. The evolution continues with green bonds, sustainability-linked loans, and warehouse facilities that aggregate smaller projects for institutional scale.

These models didn’t just finance projects—they created a replicable blueprint that’s accelerating the energy transition globally. The standardization of terms, documentation, and risk allocation means capital can flow faster and more efficiently than ever before.

Investment Criteria and Due Diligence for Lower Carbon Projects

Successful deployment of lower carbon capital requires rigorous due diligence that goes far beyond traditional financial analysis. Smart investors examine multiple layers of risk and opportunity before committing resources.

Technical feasibility stands as the foundation. You’ll need engineering assessments that validate project design, equipment specifications, and performance projections. For solar installations, this means verifying panel efficiency degradation curves, inverter reliability, and grid interconnection capacity. Wind projects demand detailed wind resource studies spanning multiple years, not just promotional estimates.

Market analysis and offtake security determine whether projected revenues will materialize. Long-term power purchase agreements with creditworthy counterparties provide stability, but you’ll also need to evaluate contract terms, pricing mechanisms, and termination provisions. Projects relying on merchant pricing face different risks that require sophisticated hedging strategies.

Carbon reduction impact measurement has evolved beyond simple displacement calculations. Investors now demand verified methodologies that account for lifecycle emissions, system boundaries, and additionality. Third-party verification adds credibility and supports impact reporting to stakeholders.

Development stage matters tremendously. Early-stage projects offer higher returns but carry construction, permitting, and technology risks. Mature projects provide stable cash flows with lower return profiles. Your portfolio strategy should balance both, depending on risk tolerance and capital deployment timelines.

Management team quality can’t be overlooked. Look for developers with completed projects, not just proposals. Track records in similar geographies and technologies matter more than general renewable energy experience. Sky Solar, for instance, demonstrates how experienced teams execute multi-country strategies effectively.

Regulatory and permitting risks vary dramatically by jurisdiction. Environmental permits, grid connection agreements, and local zoning approvals all create potential delays. Experienced developers maintain relationships with authorities and build realistic timelines that account for regulatory realities.

Portfolio Diversification Strategies Across Renewable Technologies

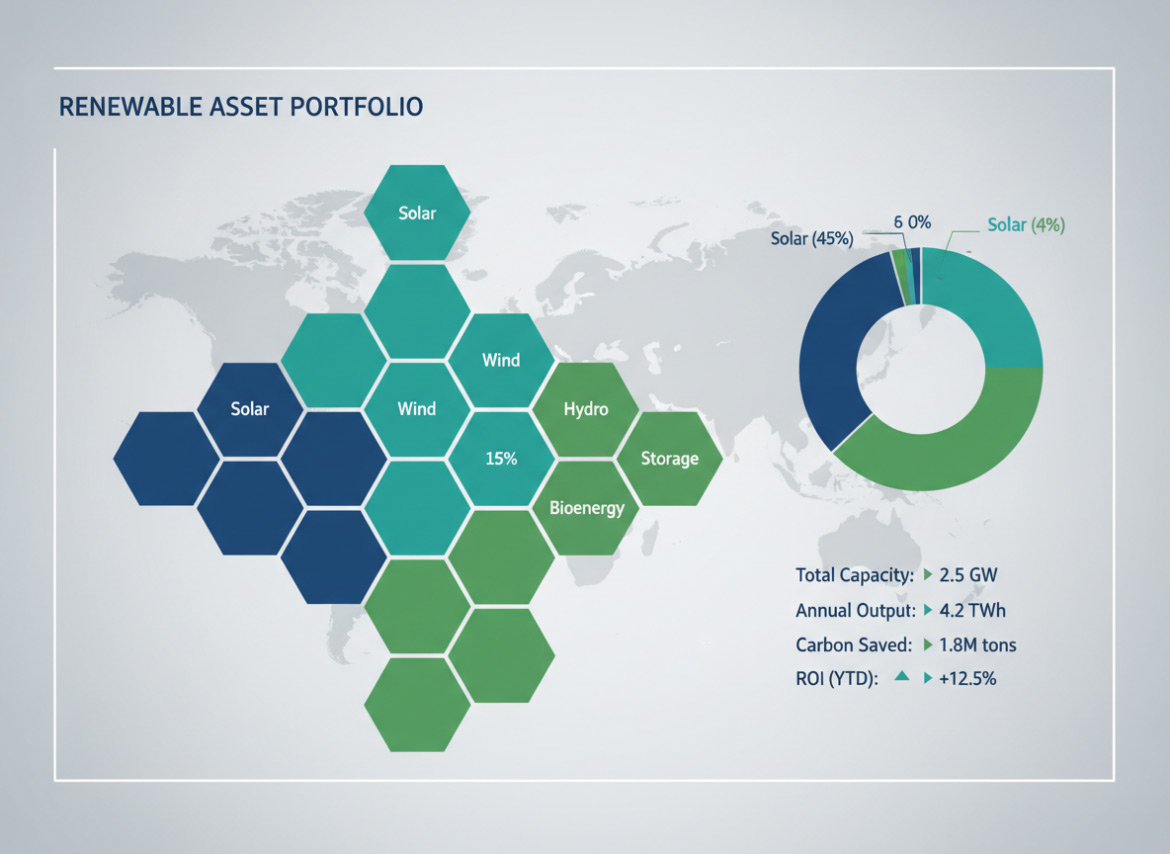

Deploying lower carbon capital effectively requires a balanced approach across multiple clean energy sectors. Rather than concentrating investments in a single technology, sophisticated investors spread risk while capturing opportunities throughout the renewable energy spectrum.

Solar PV remains a cornerstone investment, with utility-scale projects offering economies of scale and long-term power purchase agreements. Distributed generation—rooftop and community solar—provides resilience and local economic benefits. Emerging technologies like bifacial modules and perovskite cells present higher-risk, higher-reward opportunities for forward-thinking portfolios.

Wind energy continues maturing across two distinct markets. Onshore projects deliver proven returns with established supply chains, while offshore wind offers tremendous growth potential, particularly in coastal regions with favorable policy environments. The technological leap in turbine size and efficiency has dramatically improved offshore economics.

Hydroelectric power and pumped storage represent reliable baseload generation and critical grid services. Pumped hydro storage, in particular, addresses the intermittency challenge facing solar and wind deployment.

Bioenergy and sustainable bio solutions convert organic waste into renewable natural gas and liquid fuels. These technologies fill gaps where direct electrification isn’t yet feasible, especially in heavy transportation and industrial applications.

Energy storage and grid modernization investments have become essential infrastructure. Battery systems enable renewable integration while providing ancillary services that generate revenue beyond simple energy arbitrage.

Geographic diversification matters as much as technological variety. U.S. domestic markets offer regulatory stability and attractive incentives, while international opportunities—particularly in Japan’s expanding renewable sector—provide exposure to different policy frameworks, electricity prices, and growth trajectories. This multi-dimensional approach positions portfolios to weather sector-specific challenges while capturing value across the global energy transition.

Measuring Success: Performance Metrics and Impact Reporting

Successful lower carbon capital deployment requires dual accountability: financial returns and measurable environmental impact. Traditional venture capital metrics like IRR, cash-on-cash returns, and MOIC remain foundational, but they tell only half the story. Smart investors now demand comprehensive reporting that demonstrates both portfolio profitability and carbon reduction achievements.

Financial performance starts with clear benchmarks. Early-stage clean energy investments typically target IRRs exceeding 20%, while infrastructure plays—such as hydroelectric portfolios that combine stable cash flows with renewable generation—offer different risk-return profiles. What matters is setting appropriate expectations aligned with asset classes and development stages.

Environmental quantification has evolved beyond simple carbon accounting. Today’s frameworks measure avoided emissions, renewable energy generation capacity, and displacement of fossil fuel infrastructure. These metrics transform abstract sustainability claims into bankable, verifiable outcomes that satisfy both impact-focused and traditional investors.

Growth trajectories and exit outcomes validate investment theses. When portfolio companies achieve unicorn status or strategic acquisitions, they prove that lower carbon capital can generate outsized returns. These successes aren’t accidental—they reflect disciplined thesis development and operational support.

ESG reporting frameworks like SASB, TCFD, and GRI provide standardization, but transparency matters more than checkboxes. Investors increasingly expect honest assessments of challenges alongside achievements. Long-term value creation extends beyond quarterly reporting cycles, recognizing that sustainable infrastructure often appreciates over decades while generating consistent returns and measurable climate benefits.

The Future of Lower Carbon Capital Allocation

The trajectory for lower carbon capital deployment looks remarkably strong. Global renewable energy investment is projected to exceed $5 trillion by 2030, with annual flows potentially reaching $850 billion as governments and corporations accelerate decarbonization efforts. This isn’t speculative optimism—it’s driven by concrete policy frameworks and economic fundamentals.

The Inflation Reduction Act alone has unleashed hundreds of billions in domestic clean energy capital, creating predictable returns through production tax credits and investment incentives. Meanwhile, international commitments under the Paris Agreement continue strengthening, particularly across Asian and European markets where carbon pricing mechanisms make clean energy investments increasingly competitive.

Early-stage technologies represent the most exciting frontier. Next-generation battery storage, green hydrogen production, and advanced geothermal systems are attracting sophisticated investors who understand that today’s emerging technologies become tomorrow’s infrastructure. These opportunities require patient capital and technical expertise—exactly what institutional investors with long-term horizons can provide.

AI and digital technologies are transforming how we deploy and manage clean energy assets. Predictive analytics optimize grid performance, machine learning improves solar panel efficiency, and blockchain enables decentralized energy trading. These innovations aren’t futuristic concepts—they’re actively improving returns on existing portfolios.

Developing markets present compelling opportunities that many investors overlook. Sub-Saharan Africa, Southeast Asia, and Latin America face massive energy access gaps that renewables can address more cost-effectively than fossil fuel infrastructure. The insights shared at forums like the Global Energy Meet 26 highlight how international collaboration is unlocking these underserved geographies.

Institutional appetite continues expanding. Pension funds and endowments are shifting allocations as fiduciary duty increasingly encompasses climate risk management. The question isn’t whether to invest in clean energy—it’s how much and how quickly.

Partnering with Experienced Lower Carbon Capital Providers

Selecting the right capital partner can make or break a clean energy investment. It’s not just about the money—it’s about partnering with firms that bring decades of proven expertise to the table.

Look for providers with an established track record spanning multiple market cycles. They’ve weathered downturns, navigated policy shifts, and know which technologies actually deliver returns. This experience matters when you’re committing capital for the long haul.

A global network changes everything. Firms operating across 26 countries bring cross-border deal flow, regulatory insights, and connections that open doors you didn’t know existed. They’ve seen what works in Japan’s renewable markets, what’s scaling in Europe, and how to structure deals that comply with diverse regulatory frameworks.

The best partnerships feel collaborative, not transactional. You want a provider who acts as a true strategic partner—someone who’ll roll up their sleeves during due diligence, leverage their industry relationships, and provide ongoing operational guidance. Companies like HSPC demonstrate how this partnership-driven approach creates value beyond the initial capital deployment.

Access to proprietary deal flow matters tremendously. Experienced providers see opportunities months before they hit the broader market. They’ve earned co-investment rights alongside other institutional players, giving you entry into otherwise unavailable projects.

Finally, seek out thought leaders who’ve helped set industry standards. These firms don’t just follow trends—they shape them. When financial returns align with genuine mission-driven impact, you’ve found a partner who understands that lower carbon capital succeeds by doing well and doing good simultaneously.

Frequently Asked Questions

What is lower carbon capital and how does it differ from traditional energy investment?

Lower carbon capital refers to investment strategies focused on energy infrastructure, technologies, and projects that significantly reduce greenhouse gas emissions compared to conventional fossil fuel alternatives. Unlike traditional energy investment, which historically prioritized oil, gas, and coal assets, lower carbon capital targets renewable generation, energy storage, grid modernization, and efficiency technologies. The fundamental difference lies in the investment thesis: while traditional energy relies on commodity price volatility and finite resource extraction, lower carbon investments benefit from technology cost curves, policy tailwinds, and structural demand shifts toward decarbonization.

What returns can institutional investors expect from lower carbon capital allocations?

Institutional investors typically see risk-adjusted returns comparable to or exceeding traditional infrastructure investments. Operating renewable projects often generate steady, inflation-protected cash flows with 8-12% IRRs, while venture and growth-stage clean tech investments may target 15-25% returns. The key advantage is portfolio diversification—renewable assets demonstrate low correlation with fossil fuel markets and provide natural hedges against regulatory carbon risks. Hudson Sustainable Group’s portfolio companies demonstrate the breadth of return profiles available across the clean energy value chain.

How do lower carbon investments align with fiduciary responsibility?

Modern fiduciary duty explicitly requires consideration of long-term material risks, including climate-related financial exposures. Lower carbon investments address this mandate by reducing portfolio vulnerability to stranded asset risk, regulatory changes, and physical climate impacts. They’re not just ethically sound—they’re financially prudent strategies for protecting long-term capital. Many pension funds now recognize that ignoring climate risk constitutes a breach of fiduciary duty.

What are the primary risks associated with renewable energy project finance?

Key risks include technology performance, regulatory changes, offtaker credit quality, interconnection delays, and basis risk between project location and energy pricing. However, these risks are increasingly well-understood and manageable through proper due diligence, insurance products, and structured financing. The risk profile has matured significantly as the sector has scaled.

How is carbon impact measured and verified in investment portfolios?

Impact measurement relies on standardized metrics like tons of CO2 equivalent avoided, renewable energy capacity deployed (MW), and carbon intensity reduction. Third-party verification through frameworks like the Partnership for Carbon Accounting Financials (PCAF) provides credibility and consistency across portfolios.

What role do government incentives play in lower carbon capital returns?

While incentives like the Investment Tax Credit enhance project economics, mature renewable technologies increasingly compete without subsidies. Government policy creates market certainty and accelerates deployment timelines, but the fundamental economics of solar, wind, and storage now stand independently in most markets.