Understanding SFDR: The EU’s Framework for Sustainable Investment Transparency

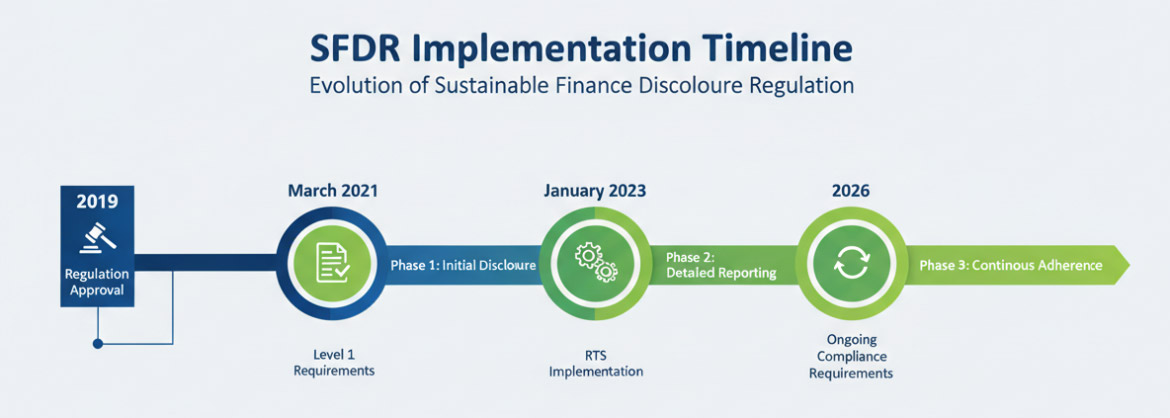

The Sustainable Finance Disclosure Regulation, better known as SFDR, represents the European Union’s ambitious effort to bring transparency and accountability to sustainable investing. Since March 2021, this regulatory framework has required financial market participants to disclose how they integrate sustainability risks and consider adverse impacts in their investment decisions.

But here’s what makes SFDR particularly significant: it’s not just another regional regulation that investors can ignore if they’re based elsewhere. The regulation applies to any financial product marketed to EU investors, which means asset managers in New York, Tokyo, or anywhere else must comply if they want access to European capital markets. That’s why institutional investors worldwide, from pension funds managing retirement assets to family offices allocating multi-generational wealth, need to understand what SFDR means for their portfolios.

At its core, SFDR tackles a problem that’s plagued sustainable finance for years: greenwashing. Without standardized disclosure requirements, financial products could claim environmental or social benefits without backing those claims with concrete data. SFDR changes that by mandating detailed disclosures at both the entity level and the product level, creating a more level playing field for genuinely sustainable investments.

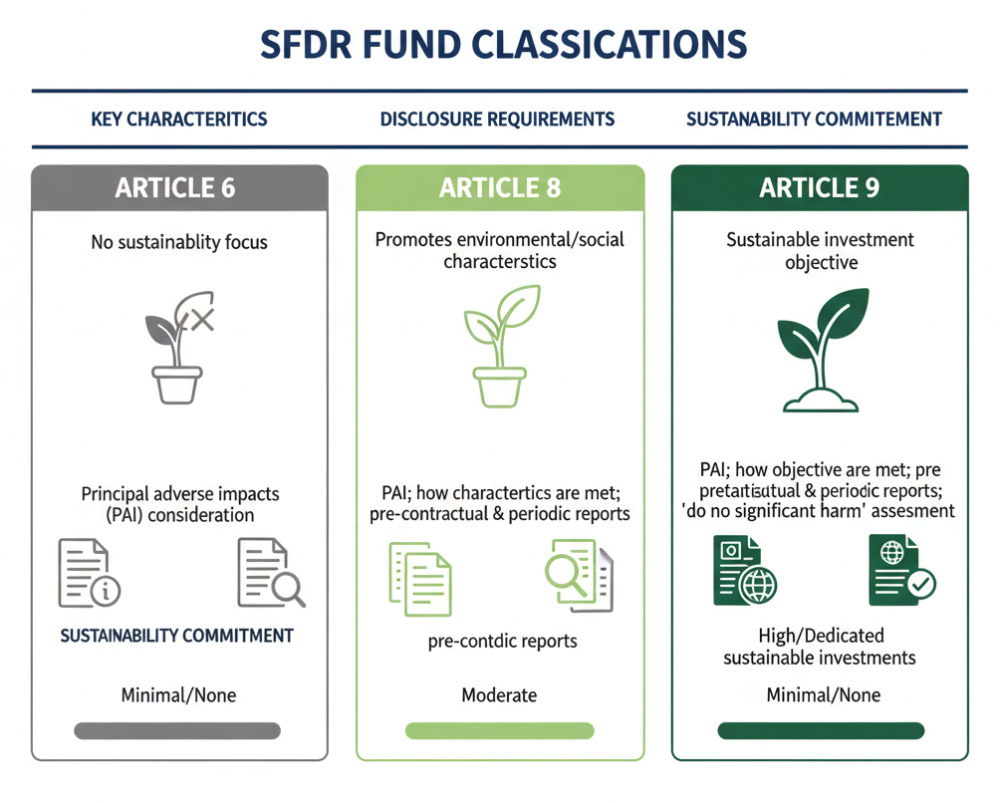

The regulation classifies financial products into three categories. Article 6 covers products that don’t promote environmental or social characteristics. Article 8 applies to products that promote these characteristics, while Article 9 designates products with explicit sustainable investment objectives. This classification system helps investors quickly assess a product’s sustainability profile and compare options.

SFDR doesn’t exist in isolation. It’s part of the EU’s broader sustainable finance ecosystem, working alongside the EU Taxonomy, which defines what qualifies as environmentally sustainable economic activities. Together, these frameworks create a comprehensive structure that’s reshaping how investors evaluate opportunities. Much like the right approach to climate and energy policy requires thoughtful implementation, SFDR demands that financial market participants think carefully about their sustainability commitments.

For investors allocating capital to renewable energy infrastructure or sustainable development projects across multiple jurisdictions, understanding SFDR has become essential. The regulation’s influence extends well beyond Brussels, setting standards that are already influencing disclosure practices globally and helping direct trillions of dollars toward genuinely sustainable investments.

SFDR Regulatory Framework: Key Requirements and Timeline

The SFDR framework operates through a tiered structure that’s evolved considerably since its initial rollout. At its core, the regulation mandates two primary disclosure levels that apply across the financial sector.

Understanding the Core Articles

Article 3 forms the foundation of SFDR’s disclosure requirements. It requires all financial market participants to explain how they integrate sustainability risks into their investment decisions. You’ll find this applies regardless of whether you’re actively marketing sustainable products. Article 4 takes this a step further by addressing principal adverse impacts (PAIs)—essentially, how investments might harm environmental or social factors. Larger firms with over 500 employees must disclose how they consider these negative impacts, while smaller organizations can explain why they’ve chosen not to.

These aren’t just theoretical disclosures. They require concrete data, methodologies, and transparent explanations that investors can actually use to make informed decisions.

The Two-Level Regulatory Approach

SFDR splits its requirements into Level 1 and Level 2 regulations. Level 1 established the broad framework and basic disclosure obligations. It set out the general principles but left room for interpretation. Level 2, delivered through Regulatory Technical Standards (RTS), filled in the details. Think of it as the difference between knowing you need to report sustainability data versus understanding exactly which 64 sustainability indicators you’ll need to track and how to calculate them.

Implementation Timeline and What Changed

The regulation kicked off on March 10, 2021, with initial requirements taking effect. Financial firms had to start classifying products and providing basic sustainability disclosures. Many scrambled to categorize their offerings as Article 6, 8, or 9 products—a classification system that’s become shorthand across the industry.

January 1, 2023, marked a significant shift. That’s when the detailed RTS requirements went live, dramatically expanding reporting obligations. Firms needed to disclose specific PAI indicators, provide more granular product-level information, and meet stricter website disclosure standards. The learning curve was steep.

Who Needs to Comply

SFDR casts a wide net. Asset managers offering investment products to European clients fall squarely within its scope. Financial advisors providing portfolio advice must comply. Institutional investors, including pension funds and insurance companies, can’t sidestep the requirements either.

Here’s what matters: even if you’re based outside the EU, SFDR likely applies to you if you’re managing money for European investors or marketing funds to EU clients. The regulation’s extraterritorial reach has surprised more than a few U.S.-based firms.

Critical Deadlines to Watch

Beyond the major 2021 and 2023 milestones, ongoing compliance requires annual updates to disclosures. Pre-contractual documents need amendments whenever product strategies shift. Website disclosures demand regular refreshes as new data becomes available. The regulatory burden isn’t one-and-done—it’s continuous and evolving as European regulators refine their expectations based on market implementation.

SFDR Fund Classifications: Articles 6, 8, and 9 Explained

The SFDR categorizes investment products into three distinct classifications based on their sustainability commitments. Think of these as a spectrum, ranging from traditional funds with minimal green criteria to products explicitly designed for environmental impact.

Article 6 funds represent the baseline category. These traditional investment products don’t promote sustainability characteristics or pursue sustainable objectives. However, they’re still subject to SFDR requirements—fund managers must disclose how they consider sustainability risks that might affect financial returns. It’s worth noting that “Article 6” doesn’t mean a fund ignores ESG factors entirely. Rather, sustainability isn’t a core part of the investment strategy. For instance, a general technology fund might hold some clean energy stocks, but that’s incidental rather than intentional.

Article 8 funds, often called “light green,” actively promote environmental or social characteristics alongside financial returns. These products integrate sustainability criteria into investment decisions without making it the primary objective. An Article 8 fund might favor companies with strong carbon reduction plans or positive labor practices. The key distinction? While sustainability matters, it’s balanced with traditional financial metrics. These funds have gained significant traction among institutional investors seeking to tilt their portfolios toward sustainability without sacrificing diversification.

Article 9 funds sit at the top tier as “dark green” investments. These products have explicit sustainable investment objectives as their core purpose. Returns matter, but the fund’s primary goal involves measurable environmental or social impact. An Article 9 renewable energy infrastructure fund, for example, might exclusively invest in solar, wind, and battery storage projects. These investments align closely with strategies supported by frameworks like the IRA clean energy tax incentives, which have accelerated institutional capital deployment into sustainable infrastructure.

The classification system directly influences capital allocation patterns. Pension funds and endowments increasingly favor Article 8 and 9 products to meet their own sustainability commitments. Family offices looking to align wealth with values gravitate toward Article 9 funds, while more cautious investors might start with Article 8 products.

Here’s what matters for your investment strategy: these classifications aren’t just regulatory labels. They signal the depth of a fund manager’s sustainability commitment and the reporting transparency you’ll receive. Article 9 funds face the strictest disclosure requirements, including detailed impact metrics and proof of sustainable outcomes. Article 8 funds must explain which characteristics they promote and how they achieve them.

Understanding these distinctions helps you match your capital to your actual sustainability goals rather than falling for surface-level green marketing.

Principal Adverse Impact (PAI) Indicators: What Investors Must Disclose

Principal Adverse Impact statements represent the SFDR’s most detailed reporting requirement, forcing financial market participants to confront the negative sustainability effects of their investments. Think of PAI indicators as a sustainability scorecard that measures how your portfolio might harm the environment or society.

At its core, PAI disclosure aims to increase transparency around investment decisions that could damage the planet or violate social norms. The regulation requires firms to explain how they’ve considered these adverse impacts when constructing portfolios and making allocation decisions.

Who Needs to Report PAI?

Here’s where company size matters. Financial market participants with 500 or more employees must publish annual PAI statements. Smaller firms can opt out, though they’ll need to explain why they’re not considering these impacts. For larger institutional investors managing billions in assets, there’s no avoiding this disclosure obligation.

The Mandatory PAI Indicators

The SFDR identifies 14 mandatory environmental and social indicators that eligible firms must report. On the environmental side, you’ll measure:

- Scope 1, 2, and 3 greenhouse gas emissions from portfolio companies

- Carbon footprint and intensity metrics

- Energy consumption and mix from non-renewable sources

- Impact on biodiversity-sensitive areas

- Water emissions and hazardous waste generation

For social and governance factors, mandatory indicators cover board gender diversity, human rights violations, and exposure to controversial weapons.

Beyond these core metrics, the regulation offers over 30 additional voluntary indicators. These cover everything from pesticide use to CEO pay ratios, letting investors demonstrate deeper commitment to sustainability measurement.

Real-World Impact on Investment Decisions

PAI reporting isn’t just paperwork—it fundamentally reshapes how institutional investors approach portfolio construction. When you’re required to disclose a renewable energy project’s impact on local biodiversity, you’ll conduct more thorough environmental assessments upfront.

Consider a pension fund evaluating two solar developments. Both offer similar returns, but one’s located near protected wetlands while the other sits on degraded agricultural land. PAI reporting pushes that environmental consideration from a nice-to-have into a quantifiable metric that affects the investment thesis.

The data requirements also create operational challenges. You’ll need robust systems to collect information from portfolio companies, many of which may lack sophisticated ESG reporting capabilities themselves. Emerging market investments often present particular difficulties, as data availability varies significantly across regions.

For renewable energy investors, PAI indicators align well with existing environmental due diligence practices. Water usage at solar panel manufacturing facilities, supply chain emissions, and end-of-life waste management for wind turbine blades—these considerations now require formal disclosure and board-level attention.

SFDR Compliance: Practical Implementation for Financial Institutions

Getting your financial institution SFDR-ready isn’t something you can accomplish overnight. The regulation demands a fundamental shift in how you collect, process, and disclose sustainability information.

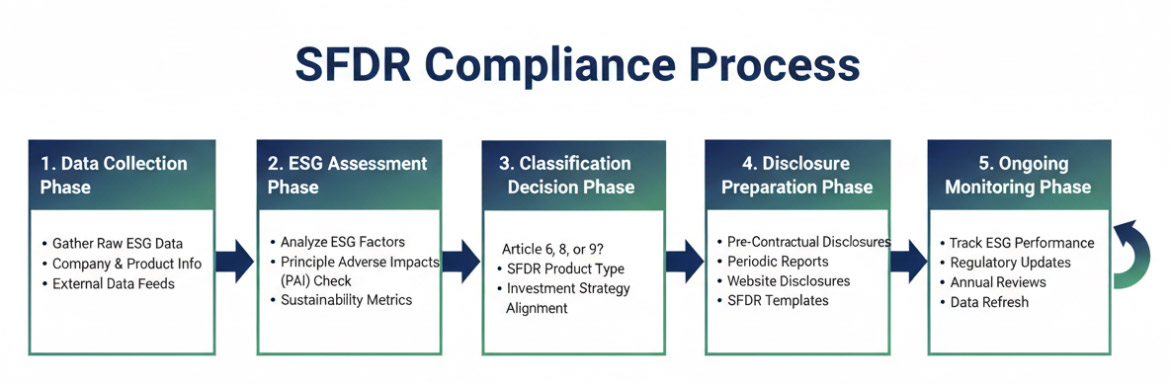

Start with a comprehensive gap analysis. Map your current ESG data infrastructure against SFDR requirements, identifying where you’re already compliant and where you’ll need to build new capabilities. Most asset managers discover they’re sitting on scattered data across multiple systems—client reporting tools here, portfolio management platforms there, and ESG research databases somewhere else entirely.

Your compliance roadmap should prioritize three foundational steps. First, classify your existing products according to SFDR articles (Article 6, 8, or 9). This classification determines your disclosure obligations and often reveals uncomfortable truths about products marketed as sustainable without proper documentation. Second, establish clear ownership across teams. SFDR compliance can’t live solely with your legal department—you’ll need collaboration between investment teams, risk management, operations, and communications. Third, set realistic timelines that account for regulatory updates, because the technical standards keep evolving.

Data collection presents the biggest headache for most institutions. You’ll need to gather information at the investee company level, often requiring direct engagement with portfolio companies. Principal adverse impact (PAI) indicators alone cover 18 mandatory metrics plus optional ones, spanning greenhouse gas emissions, biodiversity impacts, and social considerations. Many firms partner with specialized ESG data providers, but even then, you’re looking at significant data gaps—particularly for private market investments or smaller companies.

Your reporting infrastructure needs to handle both entity-level disclosures (published on your website) and product-level disclosures (included in pre-contractual documents and periodic reports). The HSPC approach demonstrates how institutional-grade frameworks can integrate sustainability metrics into investment processes, providing a model for comprehensive disclosure alignment.

Integration with existing frameworks helps streamline compliance. If you’re already reporting under TCFD, UN PRI, or other standards, you can leverage that foundation. SFDR actually complements these frameworks rather than replacing them, though you’ll need to map terminology and metrics carefully.

Technology solutions have matured rapidly to address SFDR’s complexity. Modern platforms automate data aggregation from multiple sources, calculate PAI indicators, generate disclosure templates, and maintain audit trails. The right technology investment typically pays for itself by reducing manual processes and minimizing compliance risk.

Common pitfalls? Underestimating the time required for product reclassification, failing to document methodologies clearly, and treating SFDR as a box-checking exercise rather than an opportunity to strengthen investment processes. Firms that view compliance as a strategic advantage—not just regulatory burden—tend to implement more sustainable, scalable solutions that actually enhance decision-making.

SFDR and Renewable Energy Investment: Implications for Project Finance

The SFDR framework has fundamentally reshaped how capital flows into renewable energy projects, creating both opportunities and complexities for developers and investors alike. For institutional investors evaluating solar, wind, and storage projects, SFDR classifications now serve as a screening mechanism that determines access to sustainability-focused capital pools—and often, the cost of that capital.

Article 8 and Article 9 classifications carry real weight in project finance decisions. When pension funds or family offices commit to deploying capital exclusively into Article 9 products, they’re not just making a compliance choice—they’re restricting their investment universe. Renewable energy projects that can demonstrate alignment with the EU Taxonomy’s technical screening criteria suddenly become more attractive because they unlock access to these dedicated capital streams. This isn’t theoretical; we’re seeing spreads narrow for projects with documented SFDR alignment.

The renewable energy sector benefits from a natural advantage here. Solar and wind projects typically align well with SFDR’s environmental objectives, particularly climate change mitigation. Storage projects, while newer to the taxonomy framework, are gaining recognition for their role in enabling renewable energy integration. However, qualification isn’t automatic. Projects must demonstrate compliance through detailed documentation of environmental impact, adherence to minimum social safeguards, and implementation of good governance practices.

Due diligence processes have expanded considerably. Where investors once focused primarily on technical performance, off-take agreements, and regulatory permits, they’re now scrutinizing supply chain transparency, lifecycle emissions assessments, and social impact metrics. For a utility-scale solar project, this means documenting everything from panel manufacturing provenance to decommissioning plans. It’s more work, certainly, but it’s also creating standardization that reduces information asymmetry across the market.

Institutional investors are developing sophisticated frameworks for evaluating renewable energy opportunities under SFDR. They’re asking pointed questions: Does this project meet Principal Adverse Impact thresholds? Can we verify the “do no significant harm” requirements? What percentage of revenues qualify as taxonomy-aligned? These aren’t box-checking exercises—they’re material factors in investment decisions.

For developers, SFDR compliance has become a competitive differentiator. Projects like Recurrent Energy 2 exemplify how renewable energy assets can meet rigorous sustainability standards while delivering institutional-grade returns. The developers who proactively structure projects with SFDR alignment in mind find themselves with broader access to capital and often more favorable terms.

The practical reality? SFDR has accelerated capital allocation toward renewable energy projects that can demonstrate comprehensive sustainability credentials. It’s raised the bar—but for projects that clear it, the rewards are substantial.

SFDR vs. Global Disclosure Frameworks: International Perspective

The SFDR doesn’t exist in a vacuum. It’s part of a broader global shift toward standardized sustainability reporting, though each jurisdiction has taken its own path.

In the United States, the SEC’s climate disclosure proposals (currently under regulatory review) share SFDR’s goal of transparency but take a different approach. While SFDR classifies funds into three categories and requires detailed sustainability reporting, the SEC’s framework focuses more narrowly on climate-related risks and greenhouse gas emissions. U.S. regulations emphasize materiality to financial performance, whereas SFDR takes a wider view of environmental and social impacts. The key difference? SFDR is prescriptive about product classification, while U.S. proposals center on consistent disclosure standards without categorizing investment products.

The Task Force on Climate-related Financial Disclosures (TCFD) serves as a complementary framework rather than a competing one. SFDR actually incorporates many TCFD principles, particularly around climate risk reporting. Think of TCFD as the foundational methodology for climate disclosure that SFDR builds upon. Many firms use TCFD’s four pillars—governance, strategy, risk management, and metrics—to structure their SFDR climate-related disclosures.

The UK’s Sustainability Disclosure Requirements (SDR), introduced in 2023, mirror SFDR’s labeling approach but with British refinements. The UK created its own categories: “Sustainability Impact,” “Sustainability Focus,” and “Sustainability Improvers.” Unlike SFDR’s strict Article 8 and Article 9 classifications, UK labels allow more flexibility in how funds demonstrate sustainability credentials. The SDR also places greater emphasis on anti-greenwashing measures, requiring detailed evidence backing sustainability claims.

We’re seeing clear convergence trends. The International Sustainability Standards Board (ISSB) is working to harmonize global disclosure standards, drawing from SFDR, TCFD, and other frameworks. This matters because capital flows globally, and international sustainable finance discussions increasingly address these cross-border complexities.

Why should U.S. and international investors care about SFDR despite its European focus? Three reasons: First, many global asset managers operate across borders and apply SFDR principles worldwide. Second, SFDR has become the de facto standard that other jurisdictions reference. Third, understanding SFDR helps investors evaluate European opportunities and anticipate where U.S. regulations might head. As sustainable finance evolves, familiarity with SFDR isn’t just about compliance—it’s about staying ahead of the curve.

Navigating SFDR Challenges: Greenwashing Risks and Solutions

The road to proper SFDR compliance isn’t without its hazards. Many financial institutions have stumbled—sometimes publicly—by misclassifying their products or making sustainability claims they couldn’t substantiate.

The most common pitfall? Overclassifying funds. There’s been a noticeable trend of firms initially labeling products as Article 8 or 9, only to downgrade them later when they realized they couldn’t meet the disclosure requirements. This pattern caught regulators’ attention quickly. European supervisory authorities have launched investigations into funds that marketed themselves as highly sustainable while holding portfolios that didn’t match those promises.

What constitutes greenwashing under SFDR? It’s not just outright lying. Vague statements like “we consider ESG factors” without explaining how, or cherry-picking favorable metrics while ignoring material negative impacts, will draw scrutiny. The European Securities and Markets Authority (ESMA) has made clear that marketing materials must align precisely with technical disclosures. You can’t tell investors one story and report another to regulators.

Building a defensible SFDR compliance framework starts with documentation. Every sustainability claim needs backing evidence. If you’re reporting that an investment promotes environmental characteristics, you’ll need data showing how those characteristics are measured, monitored, and integrated into investment decisions. For projects like Sky Solar, which demonstrate clear renewable energy impact, documentation becomes straightforward—the metrics speak for themselves.

Here’s what rigorous compliance looks like in practice: maintaining detailed records of due diligence processes, tracking how sustainability indicators are calculated, documenting exclusion policies and their application, and keeping audit trails of how principal adverse impact assessments inform investment decisions.

The evidence requirements extend beyond internal processes. You’ll need third-party verification for certain claims, reliable data sources for sustainability metrics, and clear methodologies that can withstand regulatory review. Many firms have learned this lesson the hard way after enforcement actions revealed gaps between their stated approaches and actual practices.

The upside? Institutions that get SFDR right gain significant advantages. Rigorous compliance signals credibility to sophisticated investors who’ve grown skeptical of generic ESG marketing. It demonstrates operational maturity and risk management capability. When your disclosures can withstand regulatory scrutiny, investors notice.

Transparency builds trust. As regulatory enforcement intensifies across Europe and similar frameworks emerge elsewhere, the firms that invested early in proper SFDR infrastructure will find themselves well-positioned. Those that took shortcuts are discovering that the reputational cost of getting it wrong far exceeds the effort of getting it right from the start.

The Future of SFDR: Upcoming Changes and Industry Outlook

The SFDR framework isn’t static. The European Commission has already launched a comprehensive review process, gathering feedback from asset managers, institutional investors, and industry bodies about what’s working and what needs refinement.

Several changes are on the horizon. Market participants have consistently flagged the complexity of current disclosure requirements, particularly around Principal Adverse Impacts (PAIs). The Commission is exploring potential simplifications that could reduce administrative burden without compromising transparency. There’s also discussion about creating clearer delineation between Article 8 and Article 9 products—many investors find the current boundaries too ambiguous.

Additional requirements are under consideration as well. The Commission is evaluating whether to mandate specific sustainability thresholds for Article 8 funds and whether to introduce standardized impact metrics that would make product comparisons more straightforward. Some stakeholders are pushing for enhanced verification requirements to address concerns about greenwashing.

Beyond Europe’s borders, SFDR is already influencing regulatory thinking worldwide. Jurisdictions from Asia to North America are watching closely, using SFDR as a blueprint while adapting frameworks to their own markets. This creates both challenges and opportunities for institutional investors with global portfolios—you’ll need to navigate multiple disclosure regimes, but there’s also potential competitive advantage for those who master sustainability reporting.

For forward-thinking institutions, the evolving SFDR landscape presents significant opportunities. Organizations that invest in robust data infrastructure and transparent reporting now will be well-positioned when regulations tighten. You’ll have a head start on peers who are still catching up.

There’s also reputational benefit. Investors who demonstrate SFDR excellence signal their commitment to sustainable finance, which increasingly matters to beneficiaries, clients, and partners. Companies like Horizon Wind Energy show how renewable infrastructure aligns with these disclosure standards while delivering returns.

The regulatory trajectory is clear: SFDR will become more refined, potentially more demanding, but also more influential globally. Institutional investors who embrace these standards rather than treating them as compliance exercises will find themselves at the forefront of the sustainable finance transition. That positioning matters, not just for regulatory compliance, but for accessing the most promising investment opportunities in the energy transition.

Frequently Asked Questions About SFDR

What does SFDR stand for and what is its purpose?

SFDR stands for Sustainable Finance Disclosure Regulation. The European Union introduced this framework to combat greenwashing and create transparency in sustainable investing. Its primary purpose is to standardize how financial market participants disclose ESG information, making it easier for investors to compare products and make informed decisions. Think of it as nutrition labels for investment funds—it tells you what’s actually inside.

Who needs to comply with SFDR regulations?

Financial market participants operating in the EU must comply, including asset managers, investment advisors, pension funds, and insurance companies offering investment products. Here’s the catch: even if you’re based outside the EU but market products to European investors, you’ll need to comply. This extraterritorial reach means SFDR’s influence extends far beyond Europe’s borders.

What is the difference between Article 8 and Article 9 funds?

Article 8 funds promote environmental or social characteristics but don’t have sustainability as their exclusive objective. They might integrate ESG factors into investment decisions or target specific outcomes like reduced carbon emissions. Article 9 funds go further—they have sustainable investment as their primary goal. These funds commit to making only investments that contribute to environmental or social objectives. It’s the difference between considering sustainability (Article 8) and making it your mission (Article 9).

Do U.S.-based investors need to worry about SFDR?

U.S. investors with European exposure should absolutely pay attention. If you’re investing in EU-domiciled funds or working with European asset managers, you’ll encounter SFDR classifications. Many U.S. institutional investors—pension funds, endowments, and family offices—have international portfolios that include European investments. Understanding SFDR helps you evaluate these holdings properly and avoid greenwashing pitfalls. Plus, as sustainable finance regulations evolve globally, familiarity with SFDR provides useful context for emerging U.S. frameworks.

How does SFDR relate to the EU Taxonomy?

The EU Taxonomy defines what counts as “environmentally sustainable,” while SFDR governs how firms disclose their adherence to these standards. They’re complementary but distinct. The Taxonomy provides technical screening criteria for activities like renewable energy generation, while SFDR requires funds to report the percentage of investments aligned with these criteria. Article 9 funds, for instance, must demonstrate how their investments align with Taxonomy objectives. This connection becomes particularly relevant when evaluating climate and energy policy implementations within investment frameworks.

What are Principal Adverse Impacts (PAIs) in SFDR?

PAIs are the negative effects that investments might have on sustainability factors. Large financial institutions must report on mandatory indicators covering issues like carbon emissions, biodiversity impact, water usage, and human rights violations. There are 18 mandatory indicators plus additional voluntary ones. This reporting forces firms to acknowledge and measure the actual environmental and social footprint of their portfolios, not just highlight the positive aspects.

How does SFDR affect renewable energy investments?

Renewable energy projects often qualify for Article 9 classification when they demonstrably contribute to climate change mitigation. However, developers and fund managers must provide detailed evidence of sustainability impact and report on PAIs. This creates more rigorous documentation requirements but also helps legitimate projects attract capital from sustainability-focused investors who need regulatory compliance.

What are the penalties for SFDR non-compliance?

Penalties vary by EU member state but can include substantial fines, reputational damage, and loss of operating licenses. National regulators have enforcement authority, and they’re increasingly scrutinizing greenwashing claims. Beyond formal penalties, non-compliance can trigger investor redemptions and damage long-term credibility—often more costly than any regulatory fine.